The idea of the first office search usually starts with a simple thought: you’ve outgrown the current setup. Maybe the team no longer fits in a home office, the coworking space that worked for two people now feels cramped, or maybe clients expect a more professional setting.

No matter what the reason is, the search can get confusing pretty fast. The market is fragmented, pricing is not always transparent, and lease terms can make two similar listings very different deals. This guide breaks the process into clear steps so you can find a space that fits your team, budget, and growth plans.

Step 1. Define Your Business Needs Before You Search

Before you compare locations or book tours, get clear on your operating needs. Otherwise, you risk wasting time on spaces that look appealing but don’t fit how your business works.

Start with a few questions:

- How many people need to use the office regularly?

- Is your team fully in-office, hybrid, or mostly remote?

- Do you need private rooms for calls, meetings, or client work?

- Will customers or partners visit the space?

- Are you expecting to grow over the next 12-24 months?

How much space do you really need?

There’s no perfect formula here, but a good starting point is to estimate how much usable space each employee needs and then add room for shared functions.

Think beyond desks. You may also need:

- A small meeting room

- A reception or waiting area

- Storage

- A kitchen or break zone

- A quiet area for focused work or calls

If your team is hybrid, you may not need a desk for every employee. Some small businesses now use a hub-and-spoke approach: a smaller central office for meetings, collaboration, and client-facing work, while employees split time between home and office. This can reduce rental costs without giving up a physical base.

Pro tip: plan for how the office will function six months from now, not just today.

Private office vs. coworking vs. serviced office: How to choose the right format

Not every business needs a traditional lease from day one. The right format depends on your size, growth stage, and need for flexibility.

- Coworking space usually works well for very small teams, solo founders, and early-stage startups. It offers low commitment, shared amenities, and fast move-in. The downside is limited privacy, less brand control, and fewer options to customize the space.

- Serviced offices sit in the middle. They typically provide furnished private suites, internet, reception services, meeting rooms, and shorter lease terms. For small businesses that want a professional setup without handling fit-out, operations, or long contracts, this is a strong option.

- Traditional office leases offer the most control. You usually get more space, more branding freedom, and potentially better long-term economics per square foot. But they also come with more responsibility and longer commitments.

Step 2. Set a Realistic Budget

Monthly rent is only part of the story. Office space can become one of the largest fixed operating expenses for a small business, so your budget has to include the full cost of occupancy. Depending on the property and lease type, you may also need to pay for:

- Utilities

- Internet

- Janitorial services

- Maintenance

- Property taxes

- Building insurance

- Parking

- Furniture and fit-out

- Security deposits

- Moving costs

First-time tenants can get caught off guard here. So a good rule is to define your maximum all-in monthly budget before you start touring spaces. Then test each listing against that number. If the real cost stretches your finances too thin, it’s the wrong office, even if the base rent looks attractive.

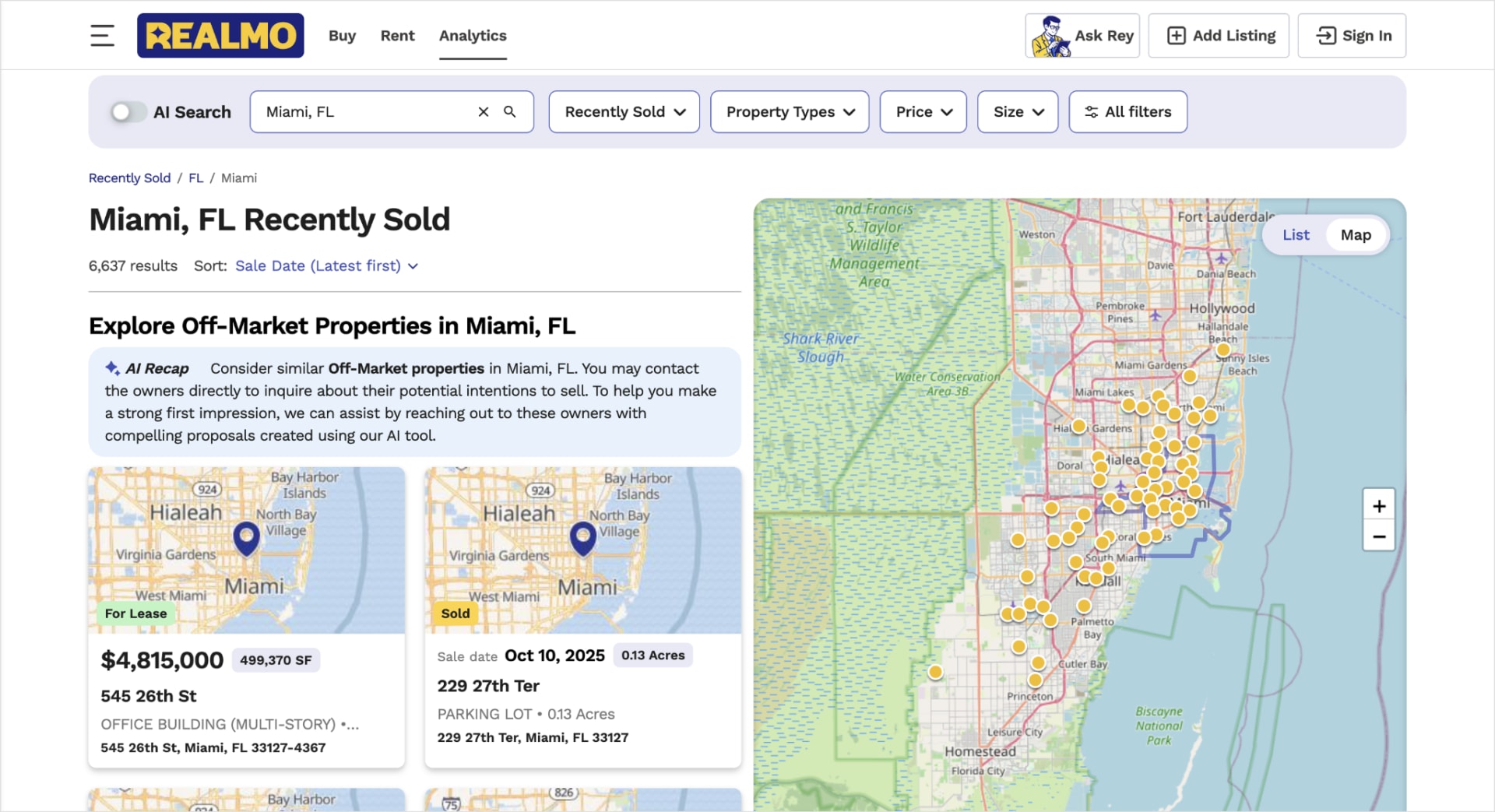

Pro-tip: To get a better sense of what the prices are like on the market in your location, use Realmo as the basis for comparative search. You can browse over 1 million listings nationwide, compare similar office spaces in your target area, and see how asking prices vary by size, location, and property type. Recently Sold adds another useful layer and shows actual nearby transactions, so you can understand the real price range in the market.

Step 3. Choose the Right Location

Location shapes your team’s daily experience, your brand perception, and your monthly costs, so convenience is just one factor. For a small business, the best location is rarely the most central or most prestigious one, but the one that makes operational sense.

Look at the location from three angles:

- Team accessibility. Can employees get there easily by car or public transportation? Is parking available? A beautiful office becomes a daily frustration if getting there is a hassle.

- Client and partner access. If people visit you regularly, the address matters more. A hard-to-find or inconvenient location can become a business problem.

- Surrounding infrastructure. Nearby cafes, banks, restaurants, gyms, and other services affect employee satisfaction and day-to-day functionality.

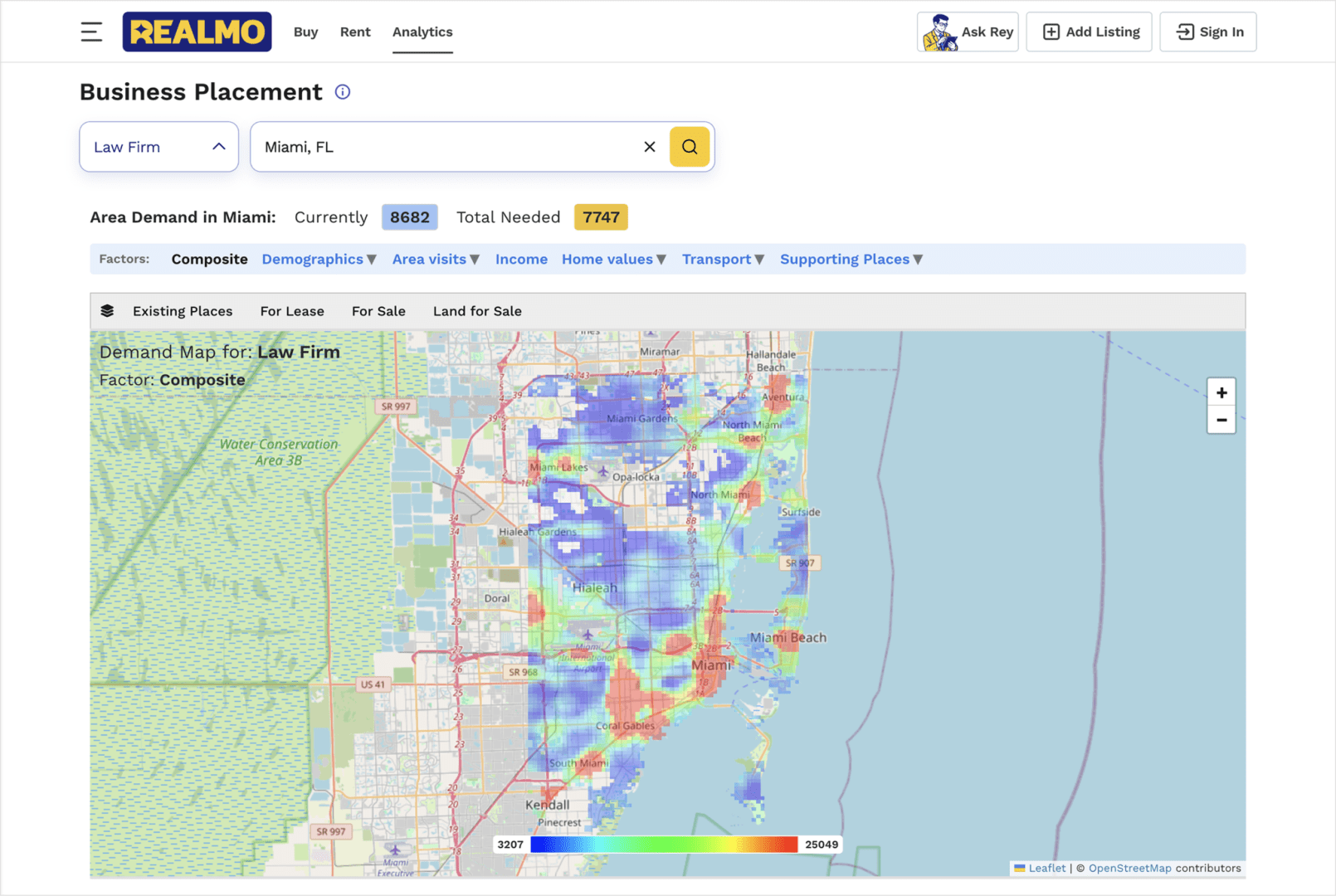

Use Realmo’s Analytics Center to do the research for you here. It helps you evaluate locations with more context before they commit. Location Intelligence lets you assess factors such as traffic, local demographics, transportation access, nearby property values, competitor presence, and supporting businesses in the area. Instead of judging a location by impression alone, you can see how it performs as a business environment.

For businesses that want a more guided starting point, Business Placement is also a helpful report. Using AI, it builds a heat map showing which areas may be the best fit for specific business types. It narrows down promising locations faster and make the search more data-driven from the beginning.

Remember: a well-connected location often creates more value than a trophy address. If a less central office gives your team a better commute, more space, easier parking, and lower rent, that may be the stronger business decision.

Step 4. Understand Your Lease Options

Before you sign anything, make sure you understand what type of commercial lease you’re looking at. This is one of the biggest sources of confusion in office rental.

The main structures small businesses should know include:

- Full-service lease. Rent usually includes many operating expenses, such as utilities, maintenance, and janitorial services. This is simpler and more predictable, which makes it attractive for smaller tenants.

- Net lease. The tenant pays base rent plus some share of property expenses. That may include taxes, insurance, or maintenance, depending on the structure.

- NNN lease (triple net). The tenant pays base rent plus property taxes, insurance, and common area maintenance. This can make the advertised rent look lower than it really is.

- Percentage lease. More common in retail than office, this structure includes base rent plus a percentage of revenue. It’s less typical for standard office users, but it’s still worth recognizing.

For a small business, lease simplicity matters. Predictable costs are often more valuable than a lower-looking base number with variable charges layered on top.

Key clauses to review before signing

Even if the rent works, the lease itself may not. Pay close attention to:

- Permitted use. Does the lease clearly allow your business activity?

- Lease term and renewal options. How long are you committing, and what happens after the initial term?

- Exit or termination clauses. Is there any flexibility if your business changes?

- Maintenance obligations. Who pays for repairs and what counts as tenant responsibility?

- Insurance requirements. Are the coverage levels reasonable for your size?

- Sublease or assignment rights. Can you sublet the space if needed?

This is the stage where a broker, attorney, or experienced advisor can save you from expensive mistakes. As a small business, you shouldn’t treat commercial leases like standard paperwork.

Why flexible lease terms matter for small businesses

Small businesses usually need more room to adapt than large companies do. You might face things like changes in headcount or, say, budget shrinkage. Flexible lease terms give you a way to respond without getting stuck in the wrong office.

For example, a serviced office with a shorter agreement may cost more per square foot than a traditional lease, but it can still be the better option if it protects you from overcommitting. On the other hand, a conventional lease with a 24-month minimum may look efficient on paper but become a burden if your team size changes, revenue fluctuates, or you pivot operations.

Step 5. Evaluate Amenities and Infrastructure

Cover the basics carefully. After all, your office space is an environment that should help teams focus on doing their jobs without distractions. Check for the following, depending on your needs:

- High-speed internet availability

- Meeting rooms

- Private call areas

- Reception or front desk services

- Kitchen or break area

- Security and after-hours access

- HVAC quality

- Cleaning and maintenance standards

- IT support or building management responsiveness

Remember to separate nice-to-haves from must-haves. A polished lobby looks great on a tour, but reliable internet and functional meeting space are way more important.

Pro tip: Create a simple checklist before each visit. If you rely on video calls, prioritize sound privacy and connection quality. If clients visit, pay more attention to reception, signage, and presentation, etc.

Step 6. Set Up the Right Search Strategy for Commercial Office Space

Once your needs are clear, your budget is realistic, and your lease criteria are defined, you can search much more efficiently. There are three main ways small businesses usually search for office space:

- Brokers. A good broker can help you navigate the market, narrow options, and negotiate terms. But this depends on how transparent the available inventory is and how broad their access is.

- Direct outreach. Some businesses contact landlords or building owners directly, especially in specific neighborhoods. This can work, but it’s time-consuming and hard to scale.

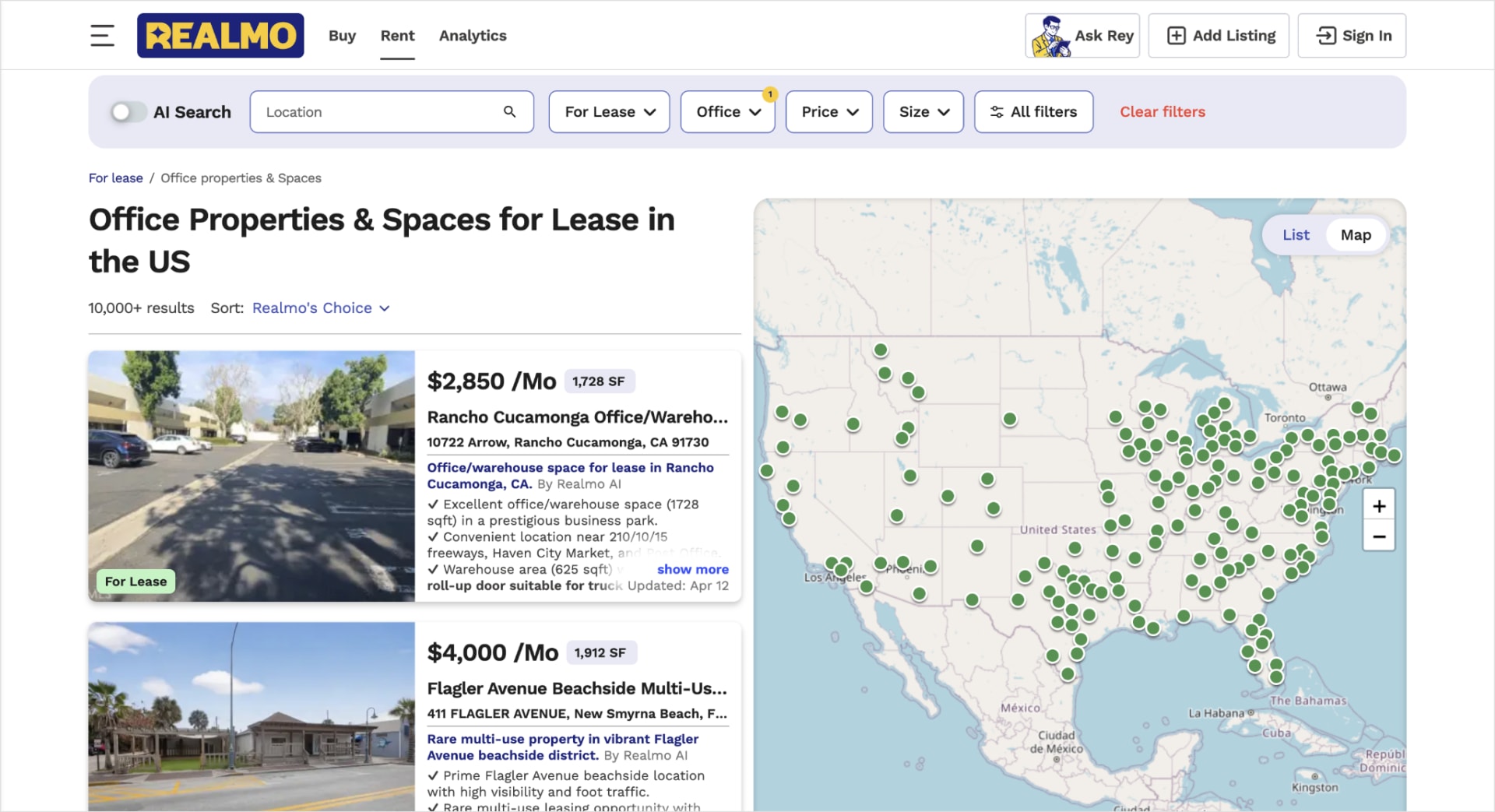

- Online listings. These are often the fastest starting point, but once again, inventory may be fragmented across platforms, and details can be inconsistent.

How Realmo helps you find the right office space

As you can see, commercial office search often lacks the structure users expect from residential real estate. There is no single universal database where every office opportunity appears in one standardized format.

Realmo solves this problem and aggregates commercial real estate listings into one easily searchable platform. You can use AI-powered search to explore office opportunities by filtering for the factors that matter in decision-making, like:

- Type of space

- Location

- Budget

- Lease-related parameters

- Property characteristics relevant to business use

In other words, you can move from broad browsing to focused evaluation much faster. Rey AI Assistant makes that process even easier to enter, especially for first-time tenants or teams without deep commercial real estate experience. You can describe what you need in plain language (for example, the type of office, preferred area, budget, team size, or lease priorities), and Rey will surface relevant options. This lowers the barrier to search, saves time, and helps businesses get to viable spaces faster without having to master CRE search logic first.

Before You Sign: The Final Checklist

Before committing to any office, run through this final checklist:

- Your business needs are clearly defined. You know how much space you need, how your team will use it, and what kind of growth you may need to accommodate over the next 12 to 24 months.

- The full budget is confirmed. You’ve calculated not just the asking rent, but the real monthly occupancy cost, including utilities, maintenance, insurance, parking, and any fit-out or move-in expenses.

- The location works operationally. Commute, parking, accessibility, and nearby services have been checked, and the area makes sense for both your team and any clients or partners who may visit.

- The office format fits your stage. You’ve chosen between coworking, serviced, or traditional space based on how your business operates today, not just what looks impressive.

- The listing holds up under closer review. At this stage, Property Insight can help you quickly assess whether a space is worth pursuing in the first place by surfacing key parameters, risks, and potential, so you can eliminate weaker options.

- The price looks reasonable for the market. With Value Estimation, you can get a clearer sense of whether the property appears fairly priced, overpriced, or has potential upside relative to the surrounding market.

- Lease terms are fully understood. You know what type of lease you’re dealing with, what is included in the base rent, and which extra costs or obligations sit on top of it.

- Key clauses have been reviewed. Permitted use, maintenance responsibilities, insurance requirements, renewal terms, and sublease rights have all been checked carefully.

- You’ve toured the space properly. You’ve seen the suite itself, the building, shared areas, infrastructure, and the general condition of the property.

- A professional has reviewed the deal. Before signing, a broker, attorney, or other experienced advisor has reviewed the lease and flagged any issues.

Final Word

Finding office space for your small business is a decision with direct impact on cost, productivity, team experience, and room for growth. The right office has to fit the way your business operates now while giving you enough flexibility for what comes next.

When you define your needs first, set a realistic budget, compare lease options carefully, and use the right search tools, the process becomes much less overwhelming. If you’re starting the search now, use Realmo.com to turn the process into a clear, data-driven roadmap that leads to the best deal quickly.

Comments

Loading comments…